When a Resort Sells a Package, Should the Full Revenue Be Recorded as Rooms Revenue?

Resort packages are a common commercial strategy in hospitality. A guest may purchase one inclusive price that covers accommodation, meals, spa treatments, excursions, entertainment, transfers, or other experiences.

From the guest’s point of view, it may look like one simple package. But from a finance and reporting perspective, the treatment is not always simple.

A key question for hotel finance teams is:

Should the full package revenue be recorded as Rooms Revenue?

The answer is: not always.

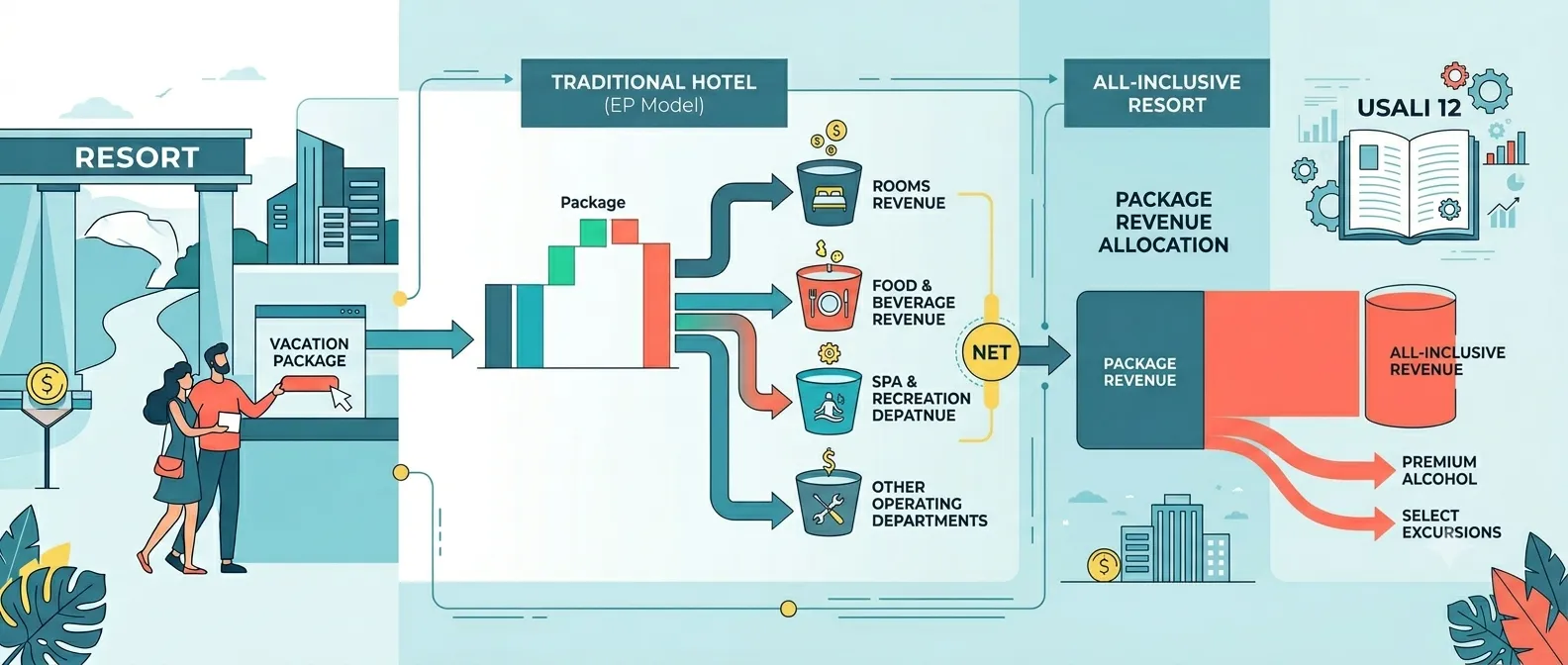

Under the Uniform System of Accounts for the Lodging Industry, 12th Revised Edition (USALI 12), the correct treatment depends on the nature of the package, the hotel’s operating model, and whether the property is operating under a traditional European Plan model or an All-Inclusive model.

1. A Resort Package Is Not Always a Room Sale

Consider a resort package that includes:

- Accommodation

- Spa treatment

- Excursion or experience

- Meals

Although the guest purchases all these services under one inclusive price, the full revenue should not automatically remain within the Rooms department.

Where interdepartmental allocation is necessary, USALI 12 explains that package revenue should be allocated among the relevant departments based on the relative standalone market values of the individual services.

This means the allocation should be based on the revenue value of each component, not its cost and not its profit margin.

For example, if a package includes room accommodation, food and beverage, and spa services, the finance team should consider the normal selling value of each service if sold separately. The package revenue is then distributed using the relative proportion of those standalone values.

2. Example: Allocation Based on Relative Standalone Market Values

USALI 12 illustrates a spa package sold for $240, where the standalone market values of the included services total $320.

| Component | Standalone Market Value | Allocation Ratio | Allocated Revenue |

|---|---|---|---|

| Room | $160 | 50% | $120 |

| Food | $112 | 35% | $84 |

| Spa | $48 | 15% | $36 |

| Total | $320 | 100% | $240 |

In this example, the guest paid $240 for a package that would normally have a standalone value of $320.

The discount is not charged entirely to one department. Instead, the package revenue is allocated proportionately across the departments based on the relative standalone market values.

Therefore:

- Rooms Revenue receives $120

- Food and Beverage Revenue receives $84

- Spa Revenue receives $36

This approach gives a fairer reflection of the value delivered by each department.

3. Applying the Same Principle to Resort Experiences and Excursions

The same principle can be applied when a resort package includes an excursion, activity, or guest experience.

For example, assume a resort sells a:

“Stay, Spa & Sunset Cruise” package

The package may include:

- Room accommodation

- Spa treatment

- Sunset cruise or excursion

In this case, the package revenue should be distributed between Rooms, Spa, and the relevant activity or excursion department based on the relative standalone selling values of each component.

This is particularly important in resorts where non-room experiences form a meaningful part of the guest journey and revenue strategy.

Examples may include:

- Sunset cruises

- Diving or snorkelling trips

- Island excursions

- Cultural experiences

- Wildlife experiences

- Cooking classes

- Wellness experiences

- Water sports activities

If these are genuine revenue-generating services included in the package, keeping the full package value within Rooms Revenue may distort the operating results.

4. What If the Excursion Is Provided by a Third Party?

Many resorts work with third-party operators for excursions, transfers, water sports, diving, or other activities.

In such cases, the contractual arrangement with the third-party provider becomes important.

The finance team should review whether the hotel is acting as:

- The principal provider of the service; or

- An agent arranging the service on behalf of a third party

This distinction can affect whether revenue is recognised gross or net for the third-party service component.

For management reporting under USALI, the key point is that the third-party service component should be recognised appropriately based on the arrangement, while the remaining package value should be allocated among the relevant hotel departments using relative standalone market values.

This prevents Rooms Revenue from being overstated and ensures that other departments or service lines are not understated.

5. Why Package Allocation Matters

Incorrect package allocation can create several reporting and management issues.

If revenue attributable to spa, excursions, food and beverage, or other services remains entirely within Rooms, the result may be:

- Overstated Rooms Revenue

- Overstated Rooms departmental profitability

- Understated Spa Revenue or Food and Beverage Revenue

- Understated performance of ancillary departments

- Distorted revenue mix analysis

- Misleading departmental benchmarking

- Poor pricing and investment decisions

- Incorrect assessment of staffing needs

For example, a resort may believe its rooms department is performing exceptionally well, while the spa or experiences department appears weak. In reality, the guest may have purchased those services as part of a package, but the revenue was never allocated to the department delivering the service.

This can lead to wrong conclusions about business performance.

6. Allocation Ratios Should Be Reviewed Regularly

USALI 12 also recommends that allocation ratios should be reviewed at least annually.

In some resort environments, more frequent review may be necessary, especially where standalone market values change materially.

This is particularly relevant for resorts with:

- High seasonality

- Dynamic room pricing

- Seasonal spa promotions

- Variable excursion pricing

- Changing guest demand patterns

- Third-party operator price changes

- Frequent package redesigns

For example, the standalone selling price of a sunset cruise may change between high season and low season. Similarly, spa treatment prices may be revised annually, while room rates may fluctuate significantly by season.

If allocation ratios are not updated, departmental revenue reporting may become outdated and unreliable.

7. Promotional Credits Are Treated Differently

USALI 12 also distinguishes package allocation from the treatment of promotional credits.

This is an important point because both may appear similar commercially, but the accounting treatment is different.

A promotional credit may allow a guest to redeem a value against a hotel service, such as:

- Spa treatment

- Food and beverage

- Retail purchase

- Resort activity

- Other hotel offering

Where a guest redeems a promotional credit for a hotel offering, the revenue generated should be recorded on a gross basis in the department providing the service, at the normal revenue value of that service.

For example, if a guest redeems a promotional credit for a spa treatment valued at $100:

- Spa Revenue is recognised at $100; and

- $100 is recorded as Promotional Credits – Contra Revenue under Miscellaneous Income – Schedule 4.

This means the promotional credit does not directly reduce Spa Revenue.

The Spa department still reflects the normal value of the service delivered. The financial impact of the promotional arrangement is separately visible through the contra-revenue account under Miscellaneous Income.

This is the USALI operating statement presentation and should be reconciled separately where statutory reporting under IFRS or U.S. GAAP requires a different revenue recognition analysis.

8. Package Allocation vs Promotional Credit Redemption

The difference can be summarised as follows:

| Area | Package Revenue | Promotional Credit Redemption |

| Nature | Guest purchases multiple services under one package price | Guest redeems a credit against a hotel service |

| Revenue treatment | Allocated among departments based on relative standalone market values | Recorded gross in the department providing the service |

| Discount / credit treatment | Package price is distributed across included components | Credit value is offset as contra revenue under Miscellaneous Income |

| Departmental visibility | Each department receives its share of package revenue | Service department records normal revenue value |

| Key objective | Fair allocation of package revenue | Preserve visibility of service activity and promotional cost |

This distinction matters because both treatments protect departmental revenue visibility.

For package revenue, the objective is to allocate the inclusive selling price fairly among the departments delivering the services.

For promotional credits, the objective is to show the value of the service delivered by the operating department while separately reporting the cost of the promotional offer.

9. Not All Hotel Packages Are Treated the Same

One of the most important points under USALI 12 is that not all hotel packages are treated the same.

This is especially important for resorts.

A package sold by a traditional European Plan hotel and a package sold by an All-Inclusive resort may look similar to the guest, but the reporting treatment can be very different.

Before deciding how to record package revenue, the finance team must first identify the business model.

10. European Plan Hotels: Allocate the Package Price

In a typical European Plan (EP) hotel, the guest may book a room-only rate and separately purchase food and beverage, spa, excursions, or other services.

If those services are included in a package, the package revenue may need to be allocated between the relevant departments based on the relative standalone market values of each component.

In other words, an EP hotel asks:

“How should we allocate the package price among the departments?”

For example, if a European Plan resort sells a weekend package including accommodation, dinner, and spa treatment, it may be inappropriate to record the full amount as Rooms Revenue.

Instead, the finance team should determine the standalone market value of each component and allocate the package revenue accordingly.

11. All-Inclusive Resorts: A Different Reporting Model

All-Inclusive resorts are different.

Under USALI 12, All-Inclusive hotels have a separate reporting approach because the business model itself is different.

In an All-Inclusive resort, the guest is not simply buying a room with optional add-ons. The guest is buying an integrated resort experience that typically includes:

- Room accommodation

- Food and beverage

- Entertainment

- Other included resort experiences

USALI 12 explains that the All-Inclusive reporting format should be used by hotels where All-Inclusive package revenue is greater than 50% of Total Revenue, calculated on a three-year rolling average.

For newly opened hotels, the format applies where All-Inclusive package revenue is forecast to exceed 50% of Total Revenue.

12. How Package Revenue Is Reported in All-Inclusive Hotels

The key difference is this:

For an All-Inclusive hotel, the package revenue is not split into Rooms Revenue, Food and Beverage Revenue, and Entertainment Revenue in the same way an EP hotel package may be allocated.

Instead, the All-Inclusive operating statement uses three main operating revenue categories:

- Package Revenue

- Nonpackage Revenue

- Miscellaneous Income

Package Revenue includes the revenue from the sale of All-Inclusive rates and other lodging packages, including:

- Room accommodation included in the package

- Food and beverage included in the package

- Entertainment included in the package

- Other services included in the All-Inclusive rate

USALI 12 indicates that Package Revenue is reported in total and is not allocated to each service within the guest package, such as rooms, food and beverage, or entertainment.

This is a major difference from the European Plan package allocation approach.

13. Costs Still Matter in All-Inclusive Reporting

Although Package Revenue is not allocated to each included service in an All-Inclusive resort, this does not mean management should ignore departmental costs.

The All-Inclusive format separately reports operating expenses such as:

- Rooms Expense

- Food and Beverage Expense

- Entertainment Expense

- Nonpackage Expense

This allows the property to calculate Package Profit and understand the cost structure of delivering the All-Inclusive experience.

For example, management may not split Package Revenue between Rooms, Food and Beverage, and Entertainment, but it still needs to understand the cost of rooms operations, food production, beverage consumption, entertainment delivery, and other included services.

Therefore, the All-Inclusive model shifts the focus from departmental revenue allocation to package profitability and cost control.

14. Nonpackage Revenue in All-Inclusive Resorts

In an All-Inclusive resort, not every revenue item is part of Package Revenue.

Nonpackage Revenue is used for goods and services that are not included in the All-Inclusive rate or are not reported as Package Revenue.

Examples may include:

- Premium food and beverage items

- Special dining experiences

- Weddings and events

- Parking and transportation

- Spa or health club services

- Golf course and pro shop revenue

- Retail sales

- Separately charged excursions

- Other chargeable services outside the package

This distinction is very important.

If a service is included in the All-Inclusive package, it may be part of Package Revenue. If it is separately charged to the guest, it may be Nonpackage Revenue and reported in the appropriate category.

15. The Key Difference: EP vs All-Inclusive

The distinction can be summarised as follows:

| Question | European Plan Hotel | All-Inclusive Resort |

| Business model | Room may be sold separately, with optional add-ons | Guest buys an integrated resort experience |

| Package revenue treatment | May be allocated among departments | Reported as total Package Revenue |

| Basis of reporting | Relative standalone market values | All-Inclusive reporting format |

| Revenue categories | Rooms, F&B, Spa, Other Operated Departments, etc. | Package Revenue, Nonpackage Revenue, Miscellaneous Income |

| Main management focus | Departmental revenue accuracy | Package profit and cost structure |

| Key question | “How should the package price be allocated?” | “What is included in the AI package and what is outside it?” |

A European Plan hotel asks:

“How should we allocate the package price among the departments?”

An All-Inclusive hotel asks:

“What is included in the All-Inclusive package, what is outside the package, and how do we report the cost of delivering the total experience?”

16. Practical Guidance for Resort Finance Teams

Before recording package revenue, resort finance teams should consider the following steps.

Step 1: Identify the Business Model

First, determine whether the property should follow a European Plan reporting approach or the All-Inclusive reporting format.

This is the most important starting point.

A package sold by an EP hotel and a package sold by an All-Inclusive resort may appear similar commercially, but the reporting treatment can be different under USALI 12.

Step 2: Identify What the Guest Purchased

Review the package inclusions carefully.

Does the package include only accommodation, or does it also include meals, spa, excursions, entertainment, transfers, or other experiences?

The finance team should not rely only on the package name. The actual inclusions matter.

Step 3: Determine Whether Departmental Allocation Is Required

For EP-style packages, determine whether revenue should be allocated among Rooms, Food and Beverage, Spa, Other Operated Departments, or other relevant departments.

If allocation is required, use relative standalone market values.

Step 4: Review Third-Party Arrangements

If the package includes services provided by third-party operators, review the contract.

Consider whether the hotel is acting as principal or agent and whether the related revenue should be recognised gross or net.

Step 5: Separate Promotional Credits from Package Discounts

Do not confuse package allocation with promotional credit redemption.

A package discount is reflected through the allocation of the inclusive package price.

A promotional credit redemption is recorded gross in the department providing the service, with the credit value reported separately as contra revenue under Miscellaneous Income.

Step 6: Review Allocation Ratios Regularly

Allocation ratios should be reviewed at least annually and more frequently where market values change materially.

This is especially important in resorts with seasonal pricing, changing package structures, or significant ancillary revenue streams.

17. Why This Matters for Hospitality Finance

Correct package revenue treatment is not just an accounting technicality.

It affects how management understands the business.

Incorrect classification can distort:

- Revenue mix

- Departmental profitability

- GOP analysis

- Ancillary revenue performance

- Labour productivity ratios

- Cost percentage analysis

- Pricing decisions

- Investment decisions

- Benchmarking against similar properties

For example, if a resort records all package revenue as Rooms Revenue, it may appear that the Rooms department is outperforming while Spa, Food and Beverage, or Experiences appear underperforming.

This could lead management to underinvest in departments that are actually creating guest value.

Similarly, in an All-Inclusive resort, incorrectly allocating Package Revenue to traditional departments may reduce comparability with the USALI All-Inclusive reporting format and distort package profitability analysis.

Conclusion

In resort finance, a package is not always simply a room sale with complimentary extras.

Sometimes, it is a combination of revenue-generating services that should be allocated among departments based on relative standalone market values.

Sometimes, it is a promotional credit arrangement where the department providing the service records gross revenue and the credit is separately reported as contra revenue under Miscellaneous Income.

And sometimes, in an All-Inclusive resort, the package is part of a different reporting model where Package Revenue is reported in total rather than allocated to each included service.

The key lesson is clear:

Before deciding how to record package revenue, first understand the business model, the package structure, and the nature of each included service.

A European Plan hotel package and an All-Inclusive resort package may look similar to the guest, but under USALI 12, the reporting treatment can be very different.

For hospitality finance teams, correct classification preserves revenue visibility, improves departmental performance reporting, supports better benchmarking, and helps management make more informed commercial decisions.

Responses