Hotel & Resort Budgeting: A Practical Guide for Building a Strong Annual Plan (USALI-Aligned)

Budgeting in hotels and resorts isn’t just an annual finance exercise – it’s the operating blueprint for the entire property. A good budget translates strategy into measurable targets, aligns department leaders, supports staffing and purchasing decisions, and protects profitability in a business where demand can shift fast.

Below is a practical, hotel-specific approach to building an accurate, usable budget—especially for full-service resorts with multiple revenue centers.

Why hotel budgeting is different

Hotels don’t budget like typical businesses because:

- Revenue is perishable (an unsold room night is gone forever).

- Demand is volatile (seasonality, events, airlift, weather, geo-political risk).

- Many costs are semi-variable (labor, utilities, linen, amenities).

- Operations are multi-department with different drivers (Rooms vs F&B vs Spa vs Activities).

- Owner, brand, and management expectations often add constraints (fees, standards, reporting).

A strong hotel budget is driver-based, not guesswork-based.

The main budget types used in hotels

- Annual Operating Budget (AOP)

The primary plan for next year’s revenue, costs, GOP, and EBITDA. - Forecast / Reforecast (monthly or quarterly)

Updates the annual view using actual performance and latest demand signals. - Rolling Forecast (e.g., 12 or 18 months forward)

Popular for resorts with volatile demand; reduces the “once-a-year” budgeting shock. - CAPEX Budget

Room renovations, plant upgrades, IT systems, soft refurbishments, and compliance projects.

The hotel budgeting workflow (a proven sequence)

1) Set the budget calendar and responsibilities

Typical timing: 8 – 12 weeks from kickoff to approval.

- Week 1–2: Assumptions + topline targets

- Week 3–5: Department submissions

- Week 6–8: Review cycles + revisions

- Week 9–10: Owner/brand review

- Week 11–12: Finalization + loading into systems

Assign ownership early:

- Revenue assumptions: Revenue Manager + DOSM + GM

- Expense and staffing: HODs with Finance control

- Consolidation & challenge: Finance

- Final approvals: GM + Owner/Asset Manager + Brand (if applicable)

Step 1: Build solid planning assumptions

These assumptions shape every line of the budget:

Commercial assumptions

- Market demand outlook (tourism trends, airlift, competitor pipeline)

- Pricing strategy (rate positioning, channel mix, discounts)

- Group vs transient mix

- Event calendar and seasonality impacts

Cost assumptions

- Wage increments, service charge expectations

- Inflation for food, beverage, utilities, chemicals

- FX rates (critical for islands/resorts with imports)

- Insurance, contracts, outsourcing costs

Operational assumptions

- Room inventory availability (renovations, out-of-order plans)

- Outlet openings/closures, concept changes

- New services (kids club, excursions, experiences)

Step 2: Revenue budgeting by department (driver-based)

A) Rooms Revenue (the engine)

Rooms should be budgeted using occupancy, ADR, and room nights, not a flat growth %.

Key drivers:

- Available rooms (after OOO/OOS)

- Expected occupancy by month

- ADR by segment (BAR, corporate, wholesale, OTA, group)

- Cancellation/no-show patterns (if significant)

- Package components (rooms vs inclusions)

Core KPIs:

- Occupancy %

- ADR

- RevPAR

- Net RevPAR (after channel costs, if you track)

B) F&B Revenue (covers + spend)

Budget outlet-by-outlet. Resorts often have:

- Buffet restaurant

- Specialty restaurants

- Bars

- In-villa dining

- Banquets/events

Drivers:

- Covers (guests × capture rate)

- Average check / spend per cover

- Meal plan structure (HB/FB/AI impacts)

- Resident vs non-resident mix (if applicable)

C) Spa / Activities / Other Operating Departments

Drivers vary:

- Spa: treatment count × average rate, therapist productivity

- Excursions: participation rate × ticket price, boat utilization

- Retail: footfall × conversion × average basket

Step 3: Expense budgeting (the part that wins or loses GOP)

A) Labor planning (the biggest cost line)

Labor should be budgeted from a staffing plan, not last year + 10%.

Approach:

- Approved org chart by department

- Manpower count by role and grade

- Salaries, allowances, benefits

- Overtime policy

- Seasonal staffing changes

- Service charge allocations (where relevant)

Helpful productivity ratios:

- Rooms: Housekeepers per occupied room, Rooms cleaned per attendant

- F&B: Covers per waiter, labor hours per cover

- Engineering: planned maintenance vs reactive workload

B) Cost of Sales (F&B cost control)

Budget food and beverage cost using:

- Menu mix and portion costs

- Vendor pricing outlook

- Import duties/logistics (for resorts)

- Wastage and spoilage targets

Use realistic targets:

- Food cost % varies by concept (buffet vs fine dining)

- Beverage cost % varies by category (wine/spirits/cocktails)

C) Other Operating Expenses (OPEX)

Common high-impact areas:

- Utilities (electricity, gas, water) – often volatile

- Laundry and linen

- Guest supplies and amenities

- Marketing and distribution costs (commissions, ads)

- Repairs & maintenance and contracts

- IT systems, licenses, connectivity

- Staff welfare, recruitment, training

Best practice: classify each cost as fixed / variable / semi-variable and budget accordingly.

Step 4: CAPEX budgeting (protect the asset and guest experience)

A resort can hit its revenue targets and still fail long-term if CAPEX is ignored.

Include:

- Mandatory compliance and life-safety projects

- Guestroom soft goods, bathrooms, HVAC, desalination, generators

- IT infrastructure and cybersecurity upgrades

- Vehicles, boats, specialized equipment

- Sustainability investments (solar, heat recovery, smart meters)

Link CAPEX planning to:

- Guest satisfaction / quality scores

- Brand standards cycles

- Asset condition surveys

- Risk and safety priorities

Step 5: Build the full P&L and validate with “sanity checks”

Once the budget is consolidated, run checks that catch unrealistic plans:

- Does occupancy align with historical seasonality and known demand events?

- Are ADR assumptions consistent with rate strategy and competitor positioning?

- Do variable costs move logically with volume (covers, occupied rooms)?

- Are departmental margins reasonable by outlet type?

- Do utility expenses match expected occupancy and operating hours?

- Is payroll consistent with the staffing plan and service level?

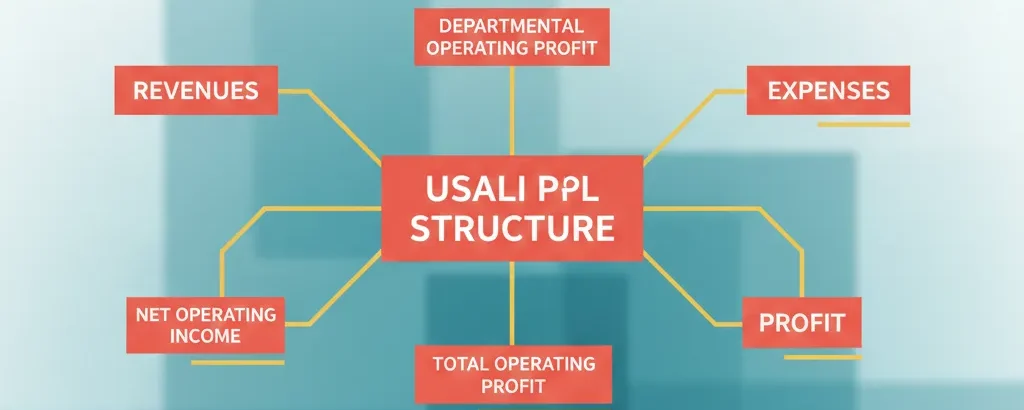

If you use USALI structure, validate by major schedules:

- Rooms, F&B, Spa/Other Ops, Admin & General, Sales & Marketing, Property Ops & Maintenance, Utilities, then GOP.

Step 6: Budget review process (make it operational, not just financial)

A budget works only if department heads believe in it and can execute it.

Strong review cycle:

- Department-by-department challenge meetings (HOD + Finance + GM)

- Document every assumption and key driver

- Final “stretch vs achievable” alignment with ownership

- Load into the accounting/reporting system with proper codes

Step 7: Monthly budget control (where budgets come alive)

A hotel budget is not a document – it’s a management rhythm.

Monthly practice:

- Flash + commentary early in the month

- Department variance analysis (volume, rate, mix, cost drivers)

- Action plan for top variances

- Update forecast based on pickup, pace, and cost changes

High-performing hotels use:

- Rolling forecast

- Scenario planning (base / optimistic / downside)

- Driver dashboards (occupancy pace, ADR, covers, labor hours)

Common budgeting mistakes (and how to avoid them)

Mistake: “Last year + 5%” budgeting

Fix: Use occupancy, ADR, covers, capture rates, and staffing drivers.

Mistake: Ignoring distribution costs

Fix: Budget commissions, channel costs, and marketing ROI by segment.

Mistake: Under-budgeting maintenance and utilities

Fix: Use trend analysis and planned maintenance schedules.

Mistake: Too many unrealistic targets

Fix: Separate stretch goals from the approved budget and track both.

Mistake: Budget is done once and forgotten

Fix: Monthly forecast discipline with clear accountability.

Tools that make hotel budgeting faster and more accurate

- PMS + RMS for demand and segment forecasting

- POS analytics for outlet-level capture and spend

- ERP / Accounting system for historical trends by account

- Excel / Power Query / Power Pivot for driver models and consolidation

- Power BI dashboards for pace, KPIs, and variance drivers

A simple “driver model” checklist (quick reference)

Rooms:

- Available rooms, occupancy, ADR, segment mix, net revenue

F&B:

- Guests in-house, capture rates, covers, average check, meal plans

Labor:

- Headcount, hours, productivity ratios, wage rates, benefits

Cost of Sales:

- Menu mix, vendor pricing, waste targets

Utilities & Maintenance:

- Occupancy-linked usage + fixed base load + planned projects

Closing thought

The best hotel budgets do two things at once:

- They’re realistic enough to manage daily, and

- ambitious enough to improve performance.

Responses