Laundry Expense Apportionment in Hotels & Resorts Under USALI

Why laundry allocation matters

Laundry is one of the quietest “big numbers” in hotel operations. It touches guest satisfaction (linen quality, towels, uniforms), impacts CPOR and department profitability, and can easily be misstated when you mix:

- guest laundry revenue activity,

- internal linen processing,

- uniform cleaning,

- and outsourced laundry invoices.

USALI’s objective is consistent: capture costs where they belong and allocate shared support costs fairly so departmental results can be compared property-to-property.

Step 1 – Decide: support department or revenue department?

Under USALI, your first decision is whether laundry is:

A) House Laundry (internal support)

If the laundry mainly processes:

- guestroom linen (sheets/towels),

- F&B linen (tablecloths/napkins),

- spa linen,

- uniforms,

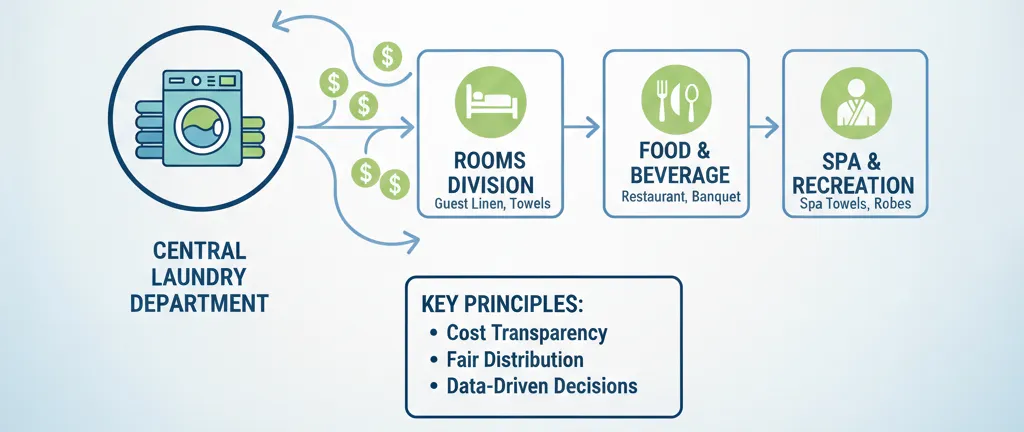

…then it functions like an internal service department and is reported as House Laundry – Schedule 12, with its cost allocated to user departments.

B) Guest Laundry / Valet (revenue-generating)

If the property sells laundry/dry-cleaning to guests as an operated activity, it can be reported within Other Operated Departments:

- Subschedule 3-X (full operated department) when material with dedicated staffing/resources

- Subschedule 3-XX (Minor Operated) when small-scale with limited structure

Practical rule: if management wants to evaluate the activity as a business (margin, staffing, pricing), treat it as an operated department; if it’s just a guest convenience with low volume, it often ends up as minor operated.

Step 2 – What goes into House Laundry (Schedule 12)?

USALI House Laundry reporting typically includes:

- Labor costs & related expenses (wages, benefits, payroll taxes, contract labor)

- Other expenses (chemicals/laundry supplies, cleaning supplies, contract services, equipment rental, training, etc.)

- Credits (e.g., cost attributable to guest/outside laundry – revenue generating)

- Allocations to user departments

And the key tie-out is:

Cost of House Laundry = Total Expenses – Credits

Net Recovery should be zero after full allocations.

This “zero out” principle is important: House Laundry is not meant to accumulate profit/loss as a service department in the internal P&L; it is meant to distribute cost to beneficiaries.

Step 3 – How allocations should work (equitable bases)

USALI repeatedly emphasizes a simple concept: allocate based on measurable usage, such as:

- Cost per pound (kg) processed

- Piece counts

- Orders processed

- Par counts (as a proxy if you can’t weigh)

Recommended approach in practice (hotel-friendly)

Use a two-driver model, because linen and uniforms behave differently:

- Linen processing allocation (Rooms, F&B, Spa, etc.)

Best drivers:

- kilograms/pounds processed by department (ideal), or

- piece counts by category (sheets, towels, napkins) when weighing isn’t reliable.

- Uniform laundry allocation (all departments)

Uniform cleaning should be charged to the department where the employees work, typically via the department’s Uniform Laundry expense line.

This avoids a classic distortion: loading all uniform cleaning into Housekeeping/Rooms just because linen “lives there.”

Recommended approach when accurate weighing isn’t always practical

In many hotels, weighing every department’s laundry output consistently is not realistic – especially when loads are mixed, peak occupancy compresses processes, or linen flows through multiple collection points. USALI’s principle still holds: the allocation must be equitable and tied to usage. When scale-based tracking isn’t feasible every day, you can still stay “USALI-aligned” by converting measurable activity into a reliable usage proxy.

A practical hybrid method: convert pieces into equivalent weight (kg/lb).

Instead of choosing either “weight” or “pieces,” treat weight as the ultimate measure and use piece counts as the measurement method:

- Create a standard weight table for common linen categories (e.g., bath towel, hand towel, bed sheet, duvet cover, napkin, tablecloth, robe).

- Track piece counts by department (Rooms, F&B, Spa, etc.) using pickup slips, laundry tags, or a simple daily/weekly log.

- Convert counts into estimated kg/lb:

Estimated weight = piece count × standard item weight - Add up each department’s total estimated weight and allocate House Laundry costs proportionally:

Department allocation % = department estimated weight ÷ total estimated weight

This method has two big advantages:

- It behaves like a weight-based allocation (which USALI prefers conceptually) without requiring a scale for every load.

- It stays consistent even when loads are mixed, because the allocation is calculated from what each department actually sent.

Controls to keep it credible

- Recalibrate standard weights periodically (e.g., monthly or quarterly): weigh a sample batch of each linen type and update the standard table if the linen quality/size changes.

- Keep categories simple: a short list of the “top movers” (sheets, towels, napkins, tablecloths) usually captures most of the volume.

- If a department has irregular items (banquet table linen, spa robes), track them as separate categories so high-impact items don’t get diluted.

Bottom line: When precise weighing isn’t practical, a “pieces → equivalent kg” conversion gives you a hotel-friendly, usage-based allocation that remains fair, auditable, and aligned with USALI’s intent.

Step 4 – Where the allocated cost appears in department P&Ls

Even when House Laundry carries the cost initially, USALI departmental guidance indicates that user departments reflect laundry charges through their own expense lines – commonly:

- Laundry & Dry Cleaning (linen processing)

- Uniform Laundry (uniform cleaning)

So operationally:

- You record costs centrally in House Laundry (Schedule 12),

- then allocate out (credit House Laundry, debit user departments’ laundry lines).

Step 5 – Guest laundry: gross vs net, and credits

USALI recognizes that guest laundry can be structured in different ways:

- in-house processing,

- outsourced processing,

- third-party concessions.

Where guest laundry is not kept as a separate operated department, USALI discusses handling guest/outside laundry through credits within House Laundry, and distinguishes treatment depending on whether you report gross or net.

Practical reporting patterns

- Guest laundry as Other Operated Department (gross reporting)

- Record guest laundry revenue + direct expenses in operated department reporting (Subschedule 3-X or 3-XX).

- If the same plant processes guest laundry, ensure House Laundry receives an appropriate credit for the portion allocated to guest laundry so you don’t double-charge internal departments.

- Guest laundry via concessionaire / outsourced

- If the property is essentially earning a commission or net share, the reporting may shift to net-style income depending on the arrangement (policy and contract specifics matter).

Step 6 – What changes in USALI 12th Edition means for laundry (effective Jan 1, 2026)

First, an important clarification:

- House Laundry – Schedule 12 is listed as “No Changes.”

However, laundry leaders will still feel the 12th edition through cross-cutting changes:

1) Utilities & sustainability tracking becomes more visible

The 12th edition strengthens consolidated reporting for energy, water, and waste and emphasizes POR metrics (e.g., water per occupied room).

Laundry is often one of the biggest operational consumers of:

- hot water,

- steam/gas,

- electricity,

- chemical discharge/waste streams.

Actionable implication: even if utilities are booked centrally, you should consider:

- sub-metering laundry,

- capturing kg processed,

- tracking water/energy per kg and per occupied room,

so you can defend your costs and spot efficiency opportunities.

2) Payroll efficiency reporting (FTE) becomes mandatory

USALI 12 introduces a mandatory Payroll FTE schedule to improve labor productivity analysis.

Laundry departments should be ready to:

- split management vs non-management hours cleanly,

- map staff to departments consistently,

- reconcile hours worked vs production volume (kg processed).

3) All-Inclusive benchmarking becomes more standardized

All-inclusive resorts now have dedicated reporting guidance to improve comparability.

Laundry isn’t singled out, but the operational reality is: AI resorts often have higher linen turnover and higher laundry intensity (covers, towels, pool linen, etc.). Better AI reporting helps owners/operators interpret laundry KPIs fairly in benchmarking.

Step 7 – Building a USALI-compliant laundry cost model (what to track)

To allocate cleanly and defend your numbers, track these monthly:

A) Production statistics (the allocation foundation)

- Total kg/lbs processed

- kg/lbs by department (Rooms, F&B, Spa, etc.)

- Uniform pieces or uniform kg by department

- Rewash/reject rate (quality driver)

B) Cost pools (what you allocate)

- Labor + payroll related

- Chemicals and laundry supplies

- Repairs/maintenance + parts

- Outsourcing/overflow laundry

- Linen rental costs (if applicable)

C) Key KPIs you can publish to HODs

- Cost of House Laundry per occupied room (CPOR)

- Cost per kg/lb processed

- Labor hours per 100 kg/lbs

- Chemical cost per kg/lb

- Rewash % (quality + cost driver)

(These align well with the 12th edition’s broader move toward more comparable operational metrics.)

Common errors (and how to prevent them)

| Errors | Fix |

|---|---|

| Uniform cleaning charged to Rooms/Housekeeping by default | charge Uniform Laundry to each department. |

| Guest laundry costs double-counted | if guest laundry revenue is reported elsewhere, House Laundry must receive appropriate credits. |

| Bad allocation drivers (Fixed %) | Fix: prefer kg/lb or piece counts; document assumptions and keep them consistent. |

| No tie-out (Schedule 12 doesn’t “zero”) | ensure allocations equal Cost of House Laundry; Net Recovery should be zero. |

Practical implementation checklist

- Define whether guest laundry is operated (3-X / 3-XX) or treated via credits/net logic.

- Choose allocation bases:

- linen: kg/lb or pieces by department

- uniforms: pieces/orders by department

- Set up Schedule 12 tie-out:

- Total expenses – Credits = Cost of House Laundry

- Cost allocated out = Cost of House Laundry (Net Recovery = 0)

- Prepare for USALI 12 adoption (Jan 1, 2026):

- map utilities/water/waste tracking processes

- implement FTE reporting discipline

Super content